Navigating the Cost of Credit in Kenya: What Your Bank is Actually Charging You

If you’re planning to take out a personal loan, business capital, or a mortgage in Kenya, the first thing you probably look at is the interest rate. But banking jargon can make it incredibly difficult to compare who is actually giving you the best deal.

Based on the latest data from the Cost of Credit portal, we’re breaking down exactly how Kenyan banks are pricing their loans right now, and which ones are currently the most (and least) expensive.

Tooling

Understand more on your loan amortisation with personal investment and loan calculators

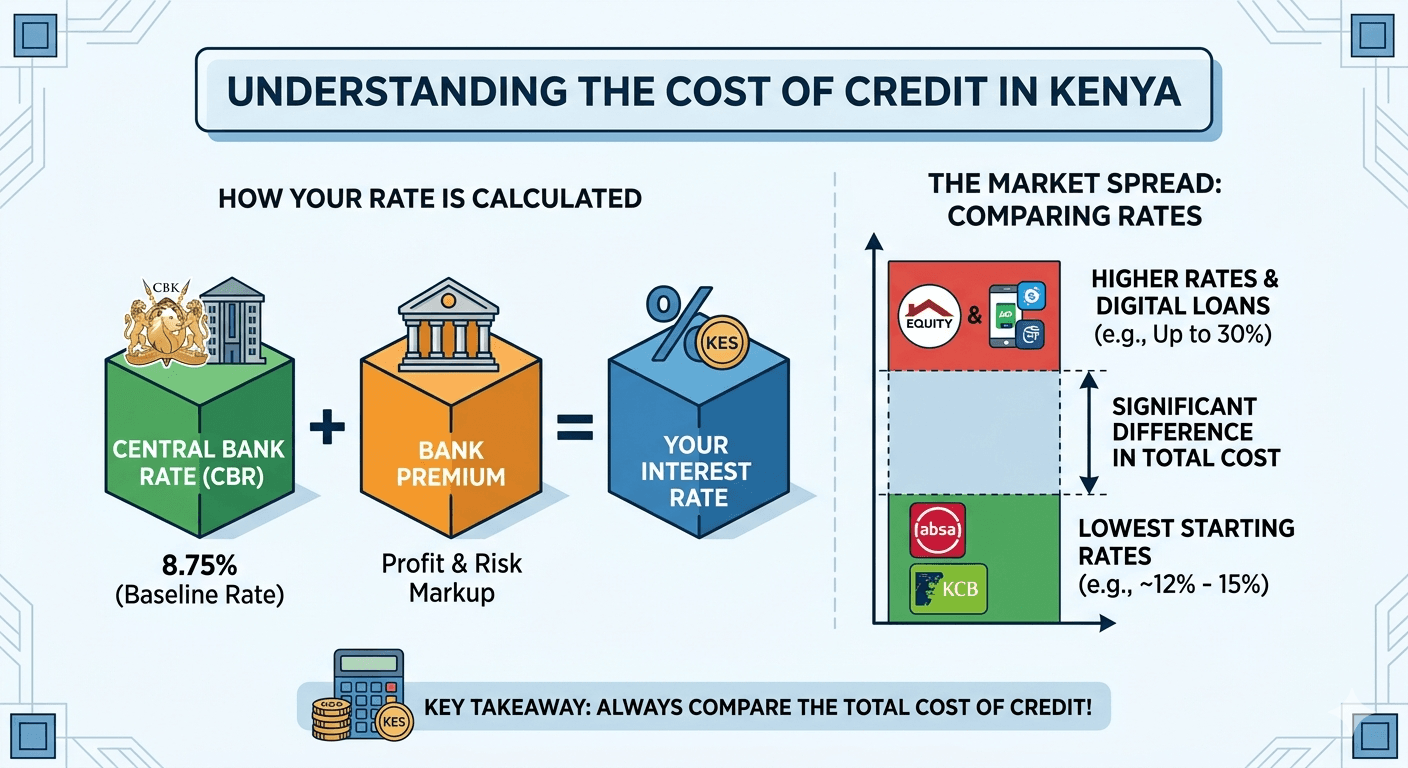

The Baseline: The Central Bank Rate (CBR)

To understand your loan’s interest rate, you have to start at the source. Currently, the Central Bank Rate (CBR) sits at 8.75%.

Think of the CBR as the baseline or the “wholesale price” of money. It’s the rate at which the Central Bank of Kenya lends money to commercial banks. When the CBR goes up, loans get more expensive. When it goes down, borrowing becomes cheaper.

The Formula: How Your Rate is Calculated

Banks don’t just lend you money at the CBR — they need to make a profit and cover the risk of you defaulting. To do this, they add a markup known as the Bank Premium.

Your final interest rate is simply:

CBR (8.75%) + Bank Premium = Your Interest Rate

(Note: A few banks, like Co-operative Bank, use the KESONIA — Kenya Shilling Overnight Rate — as their baseline, but the math works exactly the same way).

The Spread: From the Cheapest to the Most Expensive

According to the latest filings, there is a massive gap between the lowest and highest rates in the market. Depending on where you bank, you could be paying anywhere from under 12% to nearly 30% for credit.

Based on your

The Most Favorable Rates

If you have a strong credit profile, these banks currently offer some of the lowest starting premiums:

- Absa Bank Kenya Plc: Starting with premiums as low as 3.14%, Absa offers some rates around 11.89%.

- KCB Bank Kenya: With premiums starting around 6.2%, their base rates sit at approximately 14.95%.

- Co-operative Bank of Kenya: Using the KESONIA baseline (8.73%), their rates start around 15.3%.

The Higher End of the Spectrum

On the flip side, some banks and microfinance institutions are charging significantly higher premiums, often reflecting the higher risk profile of unsecured or fast-tracked digital loans:

- Equity Bank Kenya: While they have competitive starting rates, their maximum premiums push their highest interest rates up to 29.1%.

- HFC Limited: Primarily known for mortgages and property finance, their rates range steeply from 25.25% to 28.33%.

- Caritas Microfinance Bank: Premiums stretch up to 19.25%, pushing their upper-tier rates to 28%.

See how these numbers actually affect your wallet by trying out the calculator below. Play with the interest rate to see the difference between borrowing at 14% versus 28%.

Key takeaway: A 10% difference in an interest rate on a 3-year KES 1,000,000 loan will cost you hundreds of thousands of shillings in extra payments.

The Bottom Line

A bank’s advertised rate isn’t always the final rate you’ll get. The Bank Premium is heavily influenced by your personal credit score, your relationship with the bank, and the type of loan you are taking (secured vs. unsecured).

Before you sign any loan agreement, always ask your loan officer to clearly state their Bank Premium and provide you with a breakdown of the Total Cost of Credit.