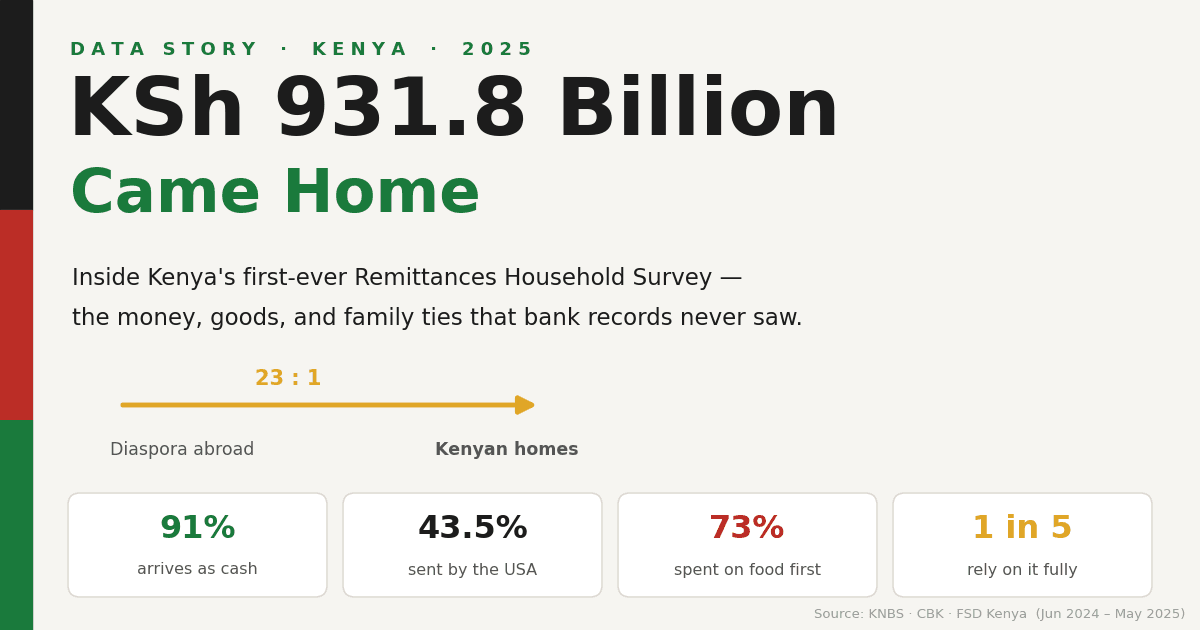

Kenya 2025: KSh 931.8 Billion Came Home: What Kenya’s First Remittances Survey Tells Us About Money and Family

A data analyst’s read of the 2025 Remittances Household Survey (KNBS, CBK & FSD Kenya)

If you grew up in Kenya, you already know the scene. A WhatsApp message at midnight: “Nimekutumia kitu kidogo, check M-Pesa.” An aunt in Dallas sending school fees. A brother in Riyadh wiring rent. A cousin in Germany shipping a laptop home before the new school term.

For the first time, somebody counted all of it.

In August 2025, the Kenya National Bureau of Statistics (KNBS), together with the Central Bank of Kenya (CBK) and FSD Kenya, ran the country’s first-ever Remittances Household Survey — knocking on doors in all 47 counties, interviewing 2,425 households, and asking a deceptively simple question: how much money and how many goods actually move between Kenyans abroad and their families back home?

The answer is staggering. Between June 2024 and May 2025, Kenyan households received KSh 931.8 billion in remittances. That’s not a typo. It’s nearly a trillion shillings — roughly the size of a national budget line — flowing in, mostly KSh 5,000 and KSh 20,000 at a time, into kitchens, classrooms, clinics, and shambas across the country.

Let me walk you through what the data says, and why it probably describes someone in your own family.

1. The big picture: a river flowing one way

The first thing that jumps out is just how lopsided the flow is.

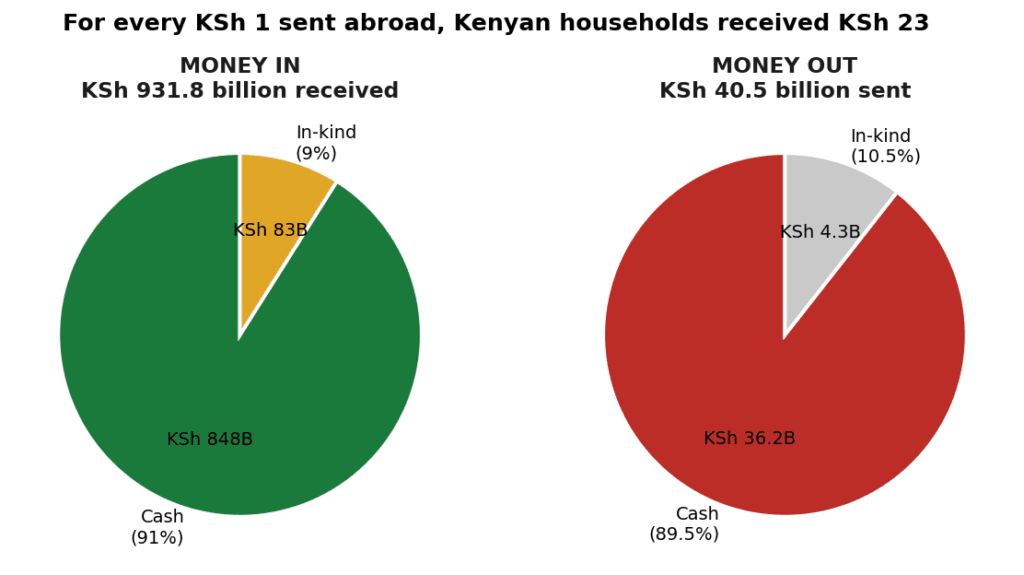

Kenyan households received KSh 931.8 billion and sent out just KSh 40.5 billion. For every single shilling that left the country, about 23 came back in. Kenya is, overwhelmingly, on the receiving end of the global money-for-family economy.

A second pattern: cash is king, but goods still matter. Of the money coming in, 91% arrived as cash and 9% (KSh 83.5 billion) arrived as in-kind — physical things. Clothes. Shoes. Phones. Laptops. Foodstuffs carried across the Busia border in a matatu. This is the part of the story that bank records have always missed, and it’s precisely why this survey matters: the official numbers, built from commercial-bank reports, never saw the suitcase full of goods that a returning relative hauls through JKIA.

Why it’s relatable: Almost everyone has received the help — or watched a parent receive it — far more often than they’ve sent it abroad. The data confirms the lived experience: money flows toward home.

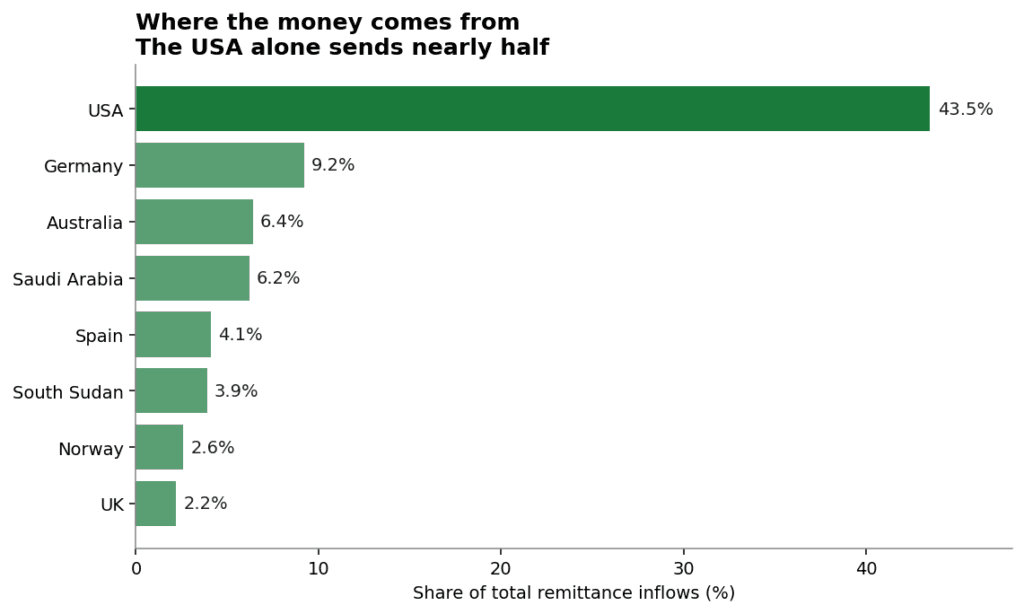

2. Where the money comes from: America carries the team

If remittances were a football match, the United States would be scoring nearly half the goals alone.

The USA sends 43.5% of everything — KSh 388 billion in cash by itself. That single corridor dwarfs everyone else. Germany and Australia follow, then a cluster of Gulf states — Saudi Arabia and Qatar — where so many young Kenyans have gone for work.

There’s a quieter sub-plot here too. South Sudan sends KSh 36 billion — more than the UK — a reminder that Kenya’s remittance map isn’t only the glamorous Western diaspora. It’s also traders, teachers, and aid workers spread across East Africa, sending food and cash back home through the Uganda and Tanzania border corridors.

One more nuance the data reveals: connection fades with each generation. First-generation migrants — people born in Kenya who left — sent KSh 797.5 billion. Their children (2nd generation) sent KSh 61.6 billion, and their grandchildren just KSh 20.2 billion. The further a family tree branches abroad, the thinner the thread back to shaggz.

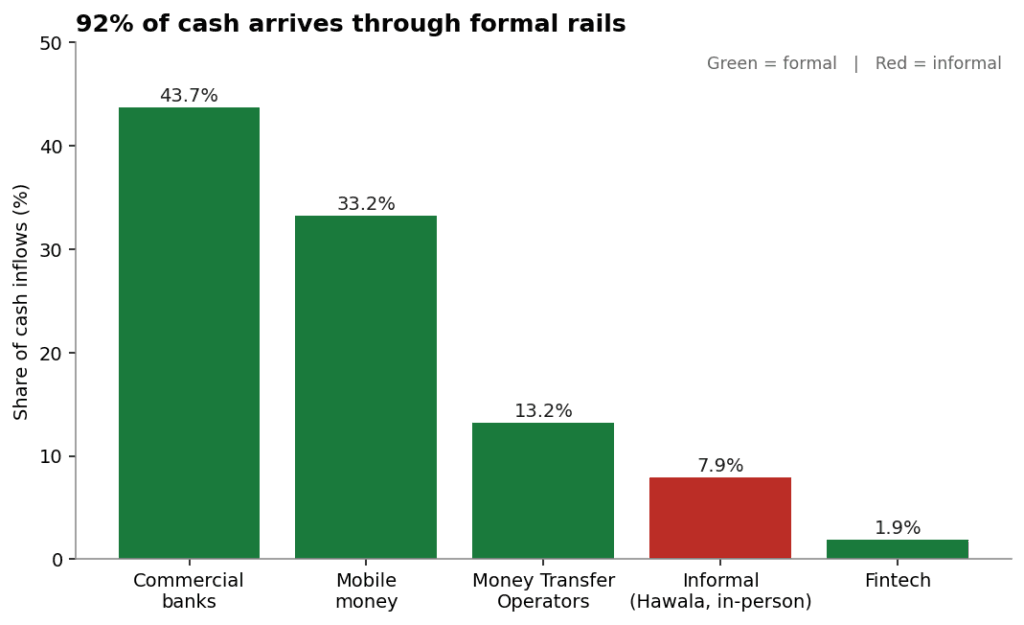

3. How the money travels: the M-Pesa generation won

Ask your parents how money used to come from abroad and you’ll hear stories of Western Union queues and forex bureaus. The data shows that world is fading fast.

Over 92% of cash now arrives through formal channels — commercial banks (43.7%), mobile money (33.2%), and Money Transfer Operators like Western Union and MoneyGram (13.2%). Kenya’s famous mobile-money rails mean a transfer from Atlanta can land in a jembe-carrying farmer’s phone in Murang’a within minutes.

And it is minutes. The survey found the USA, Saudi Arabia, and Qatar were the fastest corridors, with most transfers arriving the same day — often within the hour. The Gulf’s digital rails and Kenya’s mobile-money penetration make for a remarkably quick handshake.

Only 7.9% came through informal channels — Hawala, Hundi, or someone simply carrying cash in their pocket. These persist where they’re cheapest and most trusted, especially for in-kind goods: nearly two-thirds of physical items were hand-carried by the sender or a fellow traveller, neatly side-stepping customs and courier fees.

The catch: When asked about challenges, 83% of recipients named cost as the biggest pain. The rails are fast and formal — but fees still quietly skim value off every transfer. That’s the single clearest policy target in the whole report.

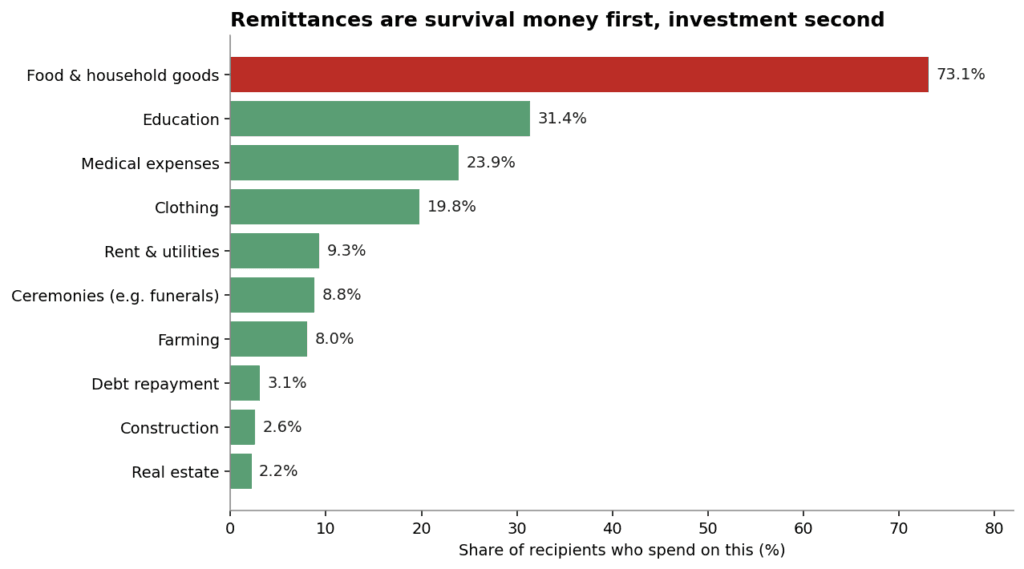

4. What the money actually buys: survival first

Here’s where the data gets personal. What do families do with the money?

The answer is humbling and unsurprising: 73% spend it on food and household goods. This is not investment capital. For most families, remittances are the difference between a full pot and an empty one.

After food comes education (31%) and medical expenses (24%) — the two great anxieties of any Kenyan household. School fees and hospital bills are exactly the emergencies that prompt that midnight “nimekutumia” message. Clothing, rent, and harambee-style ceremony contributions (think funerals and weddings) round out the list.

There’s a subtle gender story in the detail. Women recipients spend more on food (78.6% vs 66.7%) and clothing for the family, while men direct more toward education (36% vs 27%) and farming. And who decides? Mostly the people at home — recipients (49%) and household heads (32%) control the spending, while senders dictate terms only 16% of the time. The money comes with trust, not a spreadsheet.

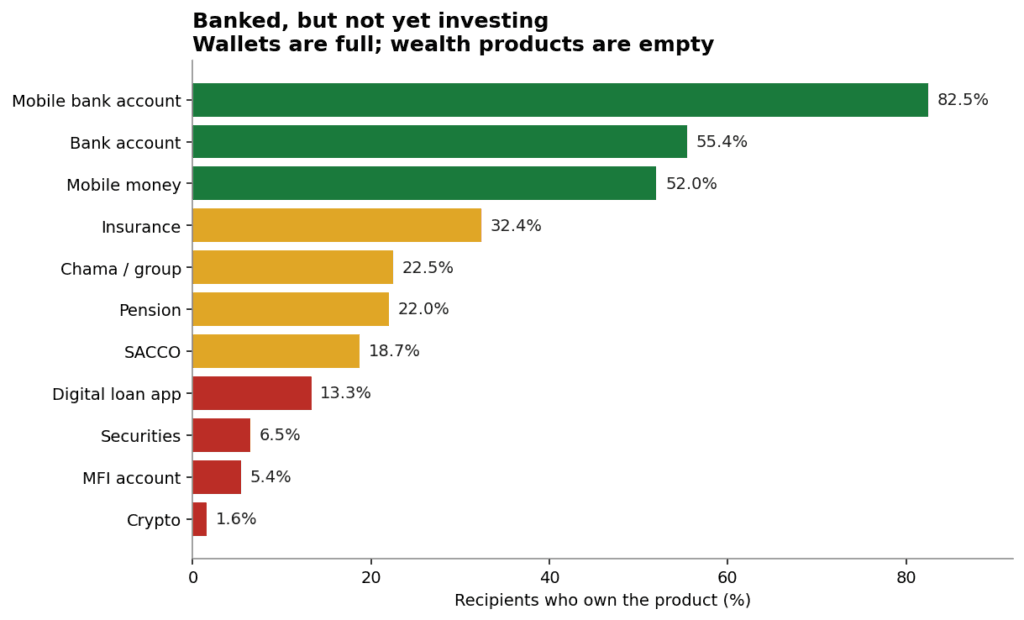

5. The opportunity hiding in plain sight: banked, but not investing

This is the chart I’d put in front of every bank executive and SACCO manager in Nairobi.

Remittance recipients are extraordinarily well-connected to basic finance — 82.5% have a mobile bank account, 55% have a traditional bank account, and 52% use mobile money. The “unbanked Kenyan” is not who’s receiving this money.

But look at the bottom of the chart. Securities: 6.5%. Microfinance: 5.4%. Crypto: 1.6%. The products that actually build wealth — shares, bonds, structured investments — are barely touched. Nearly a trillion shillings flows through hands that hold wallets but not portfolios.

This is the report’s quiet billion-shilling question: what if even a sliver of that KSh 931.8 billion were channelled into school-fee savings plans, micro-insurance, diaspora investment funds, or pay-as-you-go solar? (On that last point — only 3.6% currently spend on green tech like solar panels or efficient cookstoves, despite obvious demand.) The infrastructure for inclusion is built. The infrastructure for investment is not.

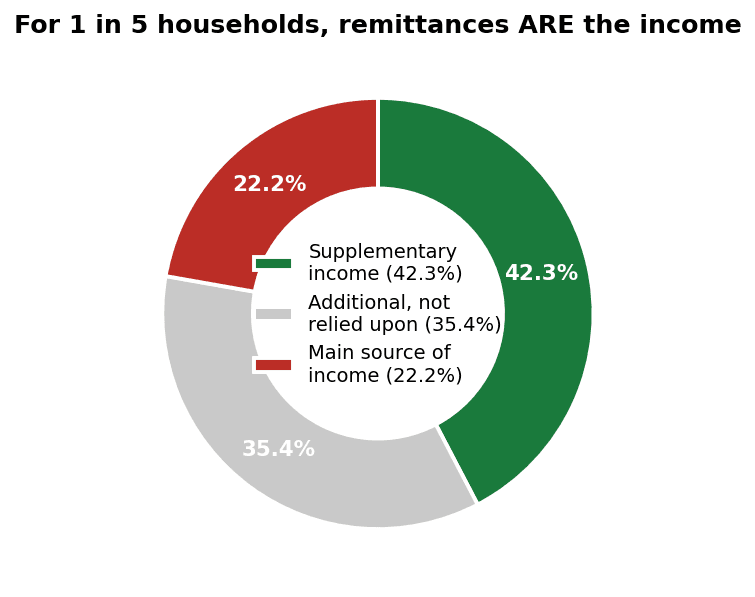

6. How much does it really matter? For 1 in 5, it’s everything

It’s tempting to think of remittances as a nice bonus — a little extra from the relative who “made it.” For many households, it is far more than that.

42% call it supplementary income, and another 35% treat it as a helpful top-up. But 22.2% — more than one in five households — say remittances are their MAIN source of income. Pull that transfer away and the lights go out, the fees go unpaid, the pot stays empty.

That’s the weight behind the number. KSh 931.8 billion isn’t an abstraction on a balance-of-payments statement. It’s the primary livelihood of millions of people.

The flows are also growing: 30% of households said they received more than the year before, mostly because relatives abroad found better jobs (“positive employment and income prospects” — cited by 64%). Only 10% saw a decline, usually from economic hardship abroad.

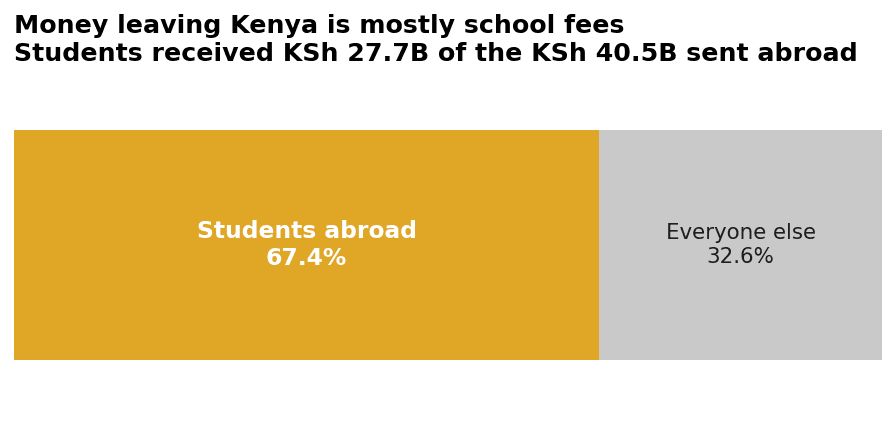

7. The flip side: money out is mostly school fees

Kenya sends far less abroad, but where it goes tells its own story.

Of the KSh 40.5 billion leaving the country, two-thirds (67.4%) went to students abroad — KSh 27.7 billion in tuition, rent, and settling-in money for Kenyans studying overseas. Parents in Nairobi wiring fees to a daughter in Manchester or a son in Australia.

The report frames this with a slightly worried tone — it’s a drain on the balance of payments — but it’s also an investment in human capital. Those students may well become tomorrow’s first-generation senders, completing the circle.

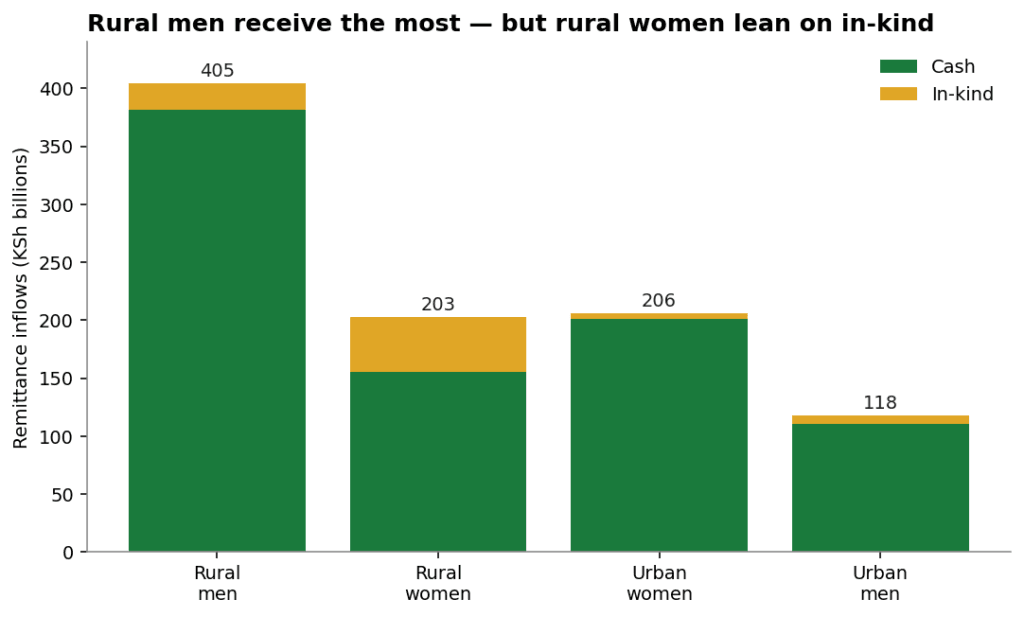

8. The rural-urban twist

One last pattern that complicates the “diaspora = city money” assumption:

Rural men receive the most money of any group (KSh 404.7 billion) — likely the shamba-owning fathers and brothers who manage family land and projects back home. But notice rural women: they receive far more in-kind support (KSh 47.5 billion) than anyone else. Where formal banking is thinner and education levels lower, families lean on goods — the clothes, food, and household items that don’t need a bank account to deliver.

Remittances, in other words, adapt to the household. Cash where there are rails; goods where there are not.

An analyst’s take away

Strip away the tables and a few clear truths remain:

- Remittances are a national-scale lifeline, not pocket money. At KSh 931.8 billion, they rival major sectors of the economy — and for 1 in 5 households, they are the economy.

- Cost is the enemy. The rails are fast and formal; the fees are the friction. A transparent, corridor-by-corridor cost dashboard (as the report itself suggests) would put shillings straight back in recipients’ pockets.

- The next frontier is investment, not access. Recipients are banked. The unmet opportunity is turning consumption into capital — savings, insurance, housing, green tech.

- The informal and in-kind flows finally have a number. That suitcase of goods, that hand-carried cash — for the first time, they’re in the official picture. Better data means better policy.

The 2025 Remittances Household Survey is, at heart, a portrait of love expressed in shillings — millions of small acts of family responsibility, finally tallied. Behind every data point is a relative who remembered home.

And the data says: home is listening for the M-Pesa beep.

Source: 2025 Remittances Household Survey Report, Kenya National Bureau of Statistics (KNBS) in collaboration with the Central Bank of Kenya (CBK) and Financial Sector Deepening Kenya (FSD Kenya). Reference period: June 2024 – May 2025. All charts created by the author from the report’s published figures.